The social media landscape

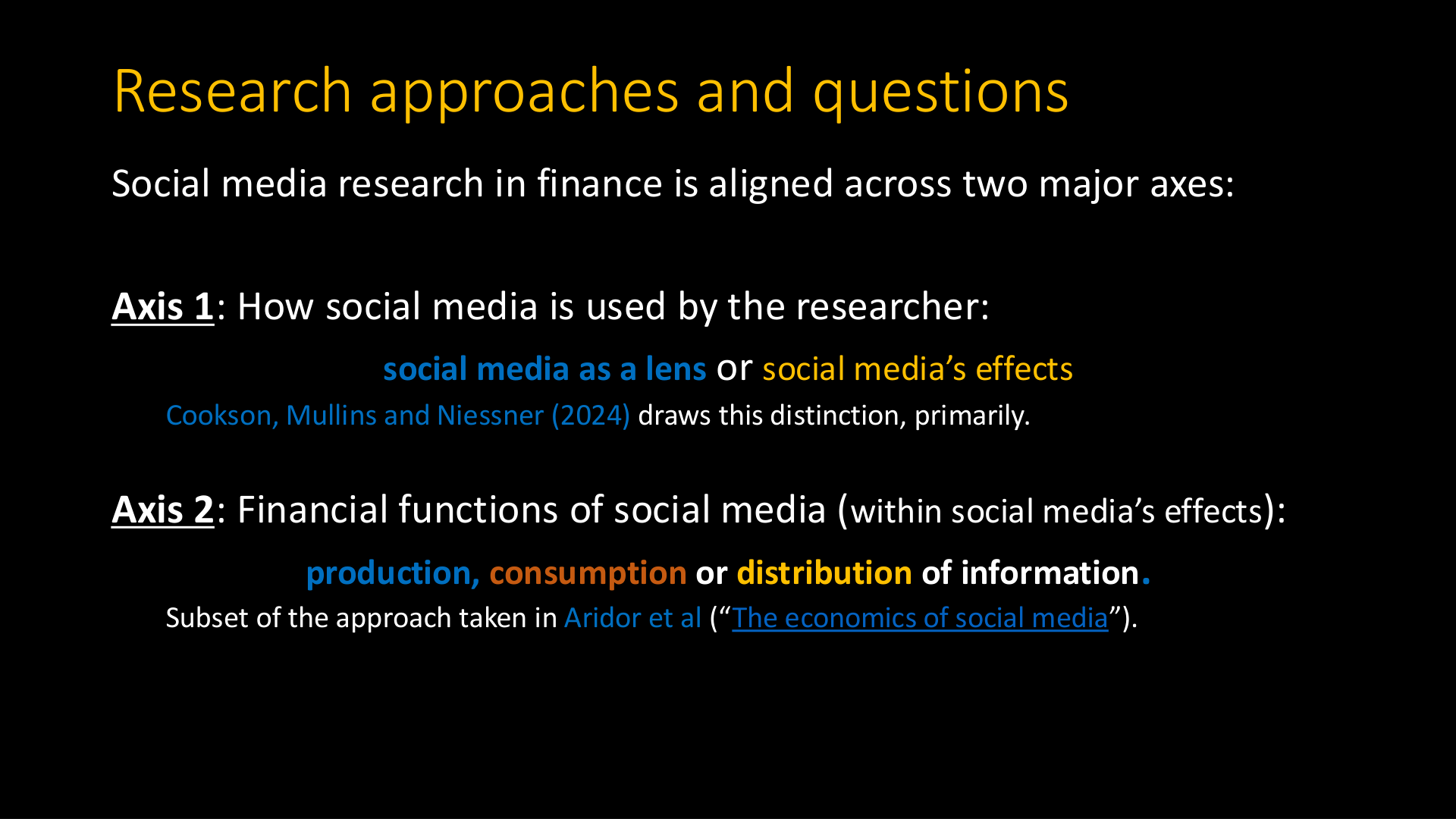

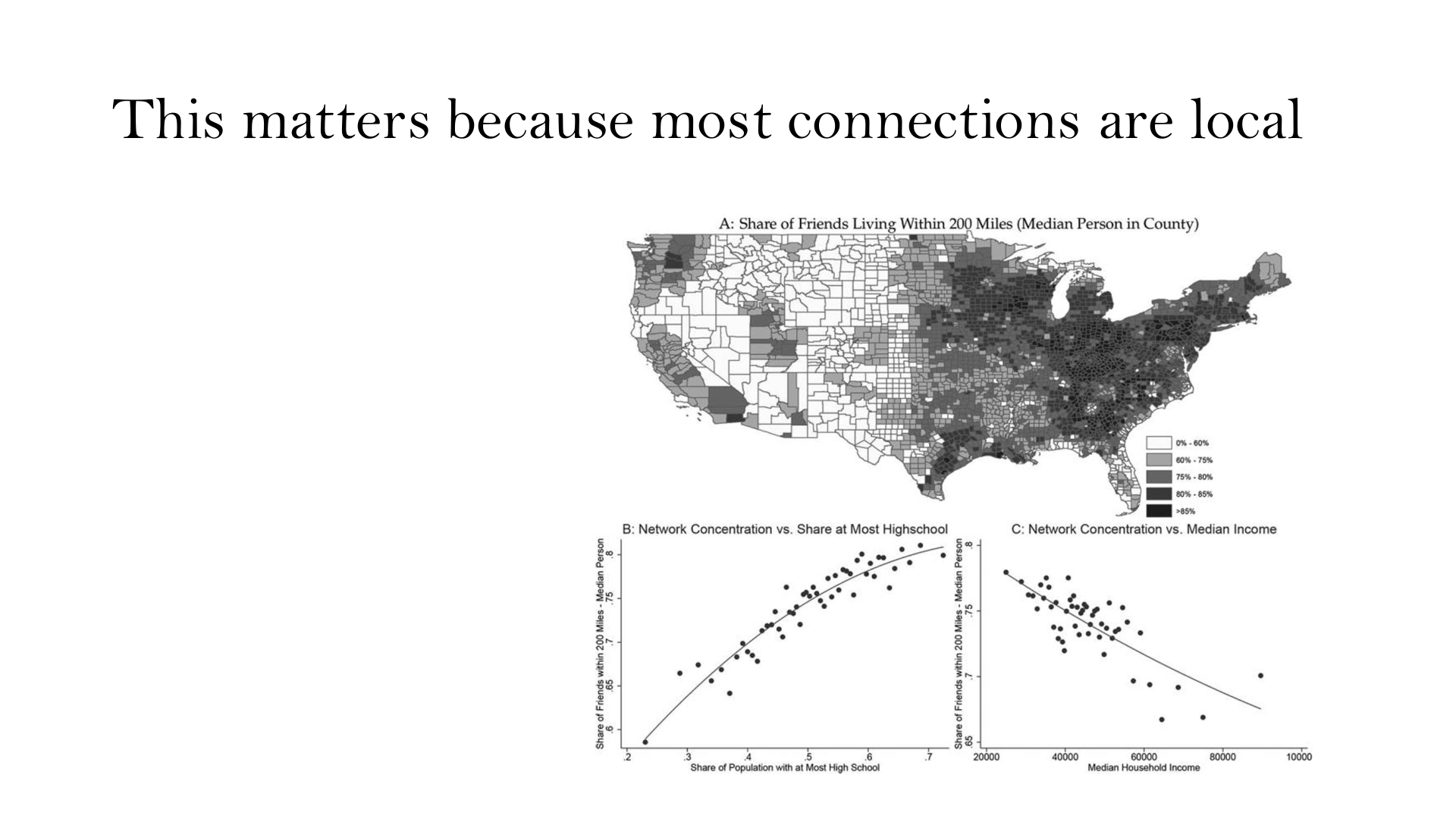

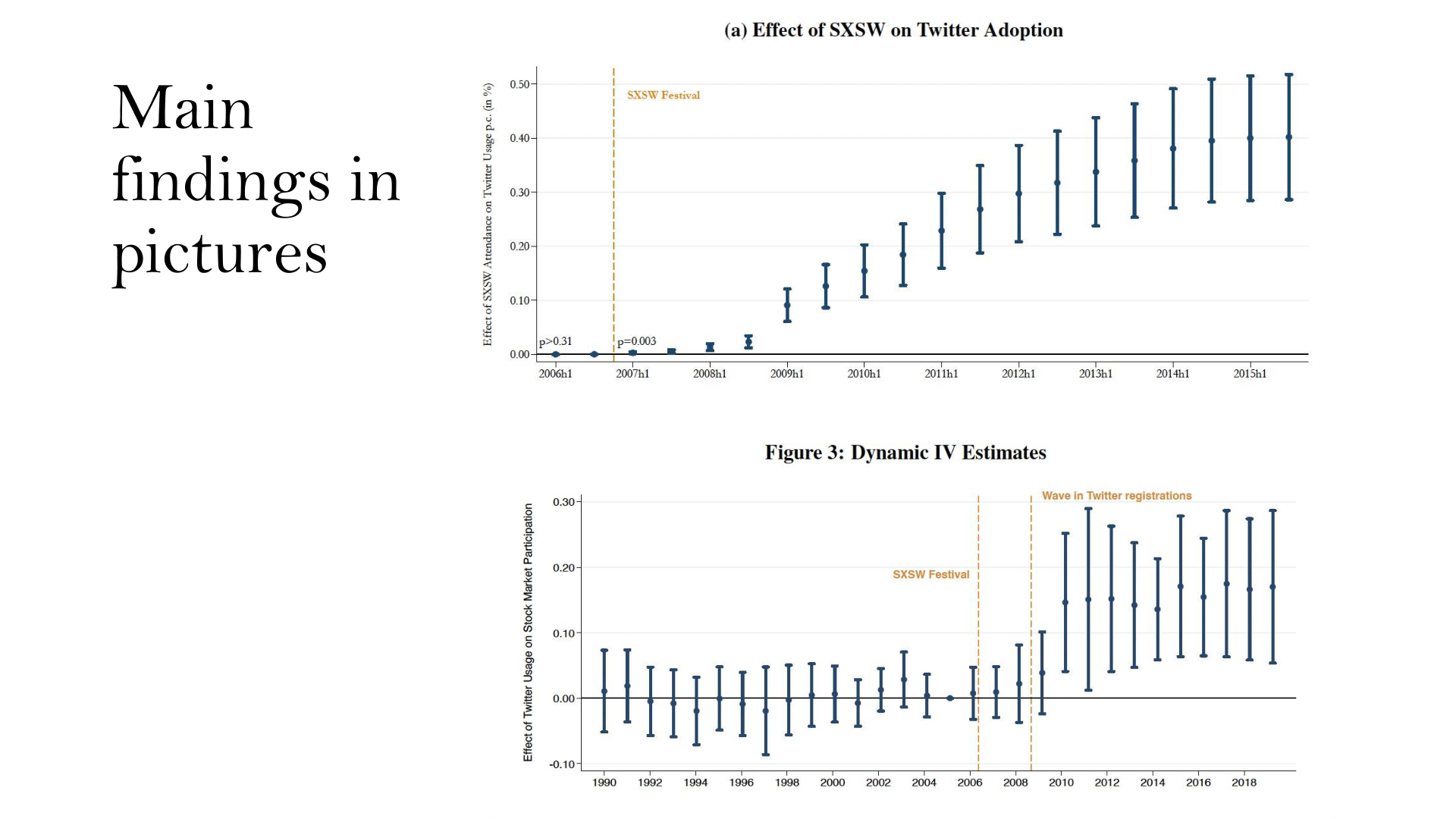

Social media has transformed how investors access information, form beliefs, and interact with markets. This session establishes the research landscape: how to think about social media data, where to find it, and what kinds of questions it can answer. The course organizes the literature along two axes — whether social media is used as a lens on investors and markets, or whether the focus is on social media's direct effects — and, within effects, whether the channel runs through the production, consumption, or distribution of financial information. Three landmark papers anchor the session. Chen et al. (2014, RFS) show that the textual content of Seeking Alpha articles predicts future stock returns, establishing that social media carries genuine signal. Bailey et al. (2018, JPE) use Facebook friendship networks to show that social connections shape real economic decisions, including house purchases and prices. Müller, Pan and Schwarz use the 2007 South-by-Southwest festival as an instrument for Twitter adoption and find that social media exposure drives stock market participation. Together, the three papers span the breadth of the field.

Key themes

- The organizing distinction: social media as a lens versus social media's effects — and within effects, the production, consumption, and distribution of financial information

- The data landscape: platform APIs, commercial products (Context Analytics, RavenPack, MarketPsych), and key public datasets

- Social media carries a signal: textual content of investor posts predicts returns; Loughran-McDonald sentiment dictionaries remain the standard

- Social networks shape economic decisions: Facebook friendship exposure predicts housing transactions and stock market participation

- Causal identification: natural experiments and instrumental variables — the SXSW shock as a model for the field

From the slides

Selected papers

- Chen, De, Hu & Hwang (2014, RFS) — Seeking Alpha and return predictability

- Bailey, Cao, Kuchler & Stroebel (2018, JPE) — Facebook connections and housing

- Müller, Pan & Schwarz (WP) — Social media and stock market participation

- Chetty et al. (2023, Nature) — Social capital and economic connectedness

- Loughran & McDonald (2011) — Sentiment word lists for finance

- Antweiler & Frank (2004) — Internet message boards and stock markets

- Cookson, Mullins & Niessner (2024) — The lens vs. effects framework

Data resources

- Social Finance Data Repository — disagreement and sentiment measures, firm-day 2010–2021

- Loughran-McDonald Master Dictionary — positive/negative word lists

- Opportunity Insights — Social Capital data (Chetty et al.)

- Context Analytics — firm-day Twitter signal (free tier for researchers)

- IRS Summary of Income (SOI) — public county and zip code data

- Müller SXSW exposure measure — county-level instrument for Twitter adoption

Social media as a lens

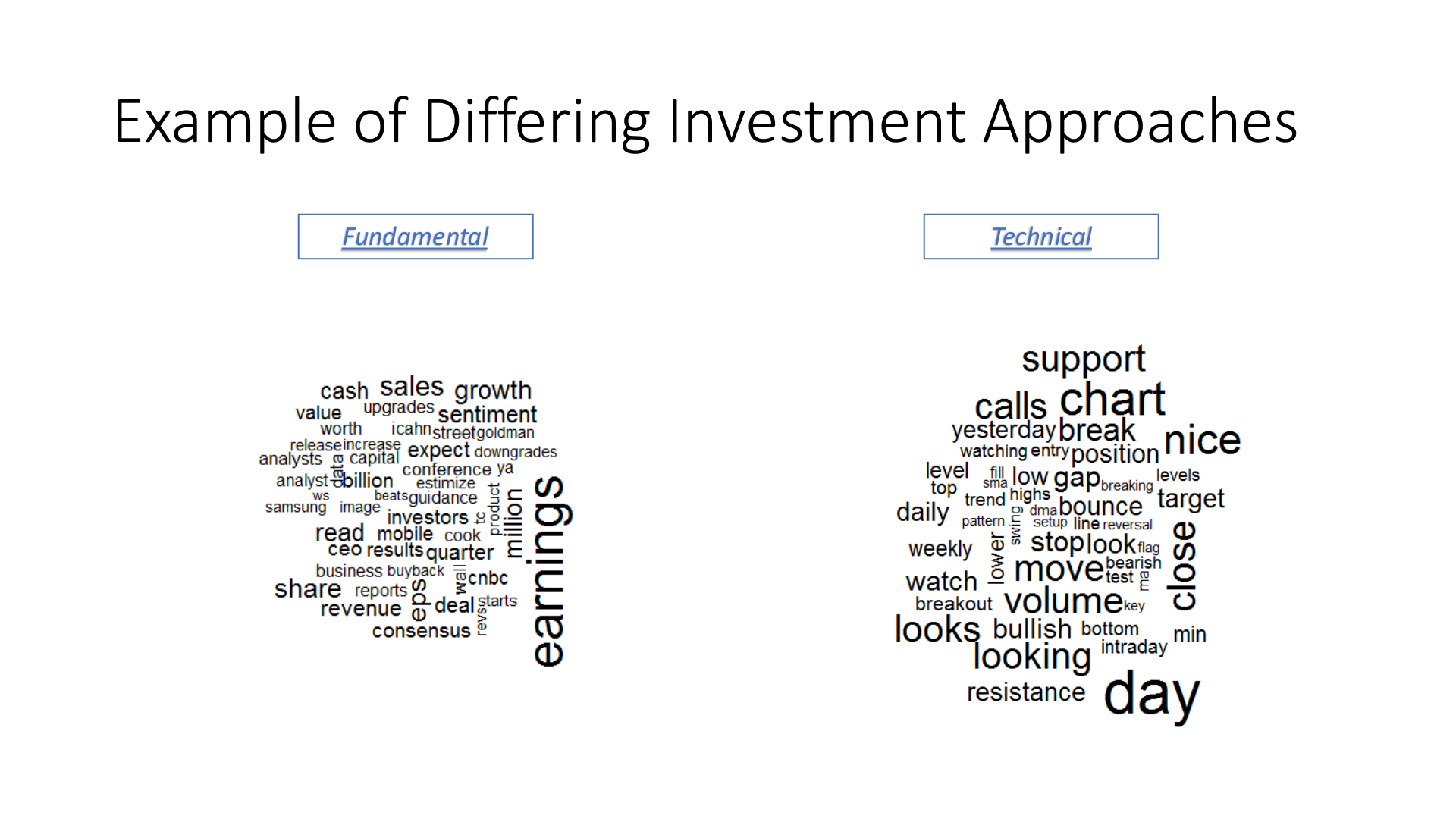

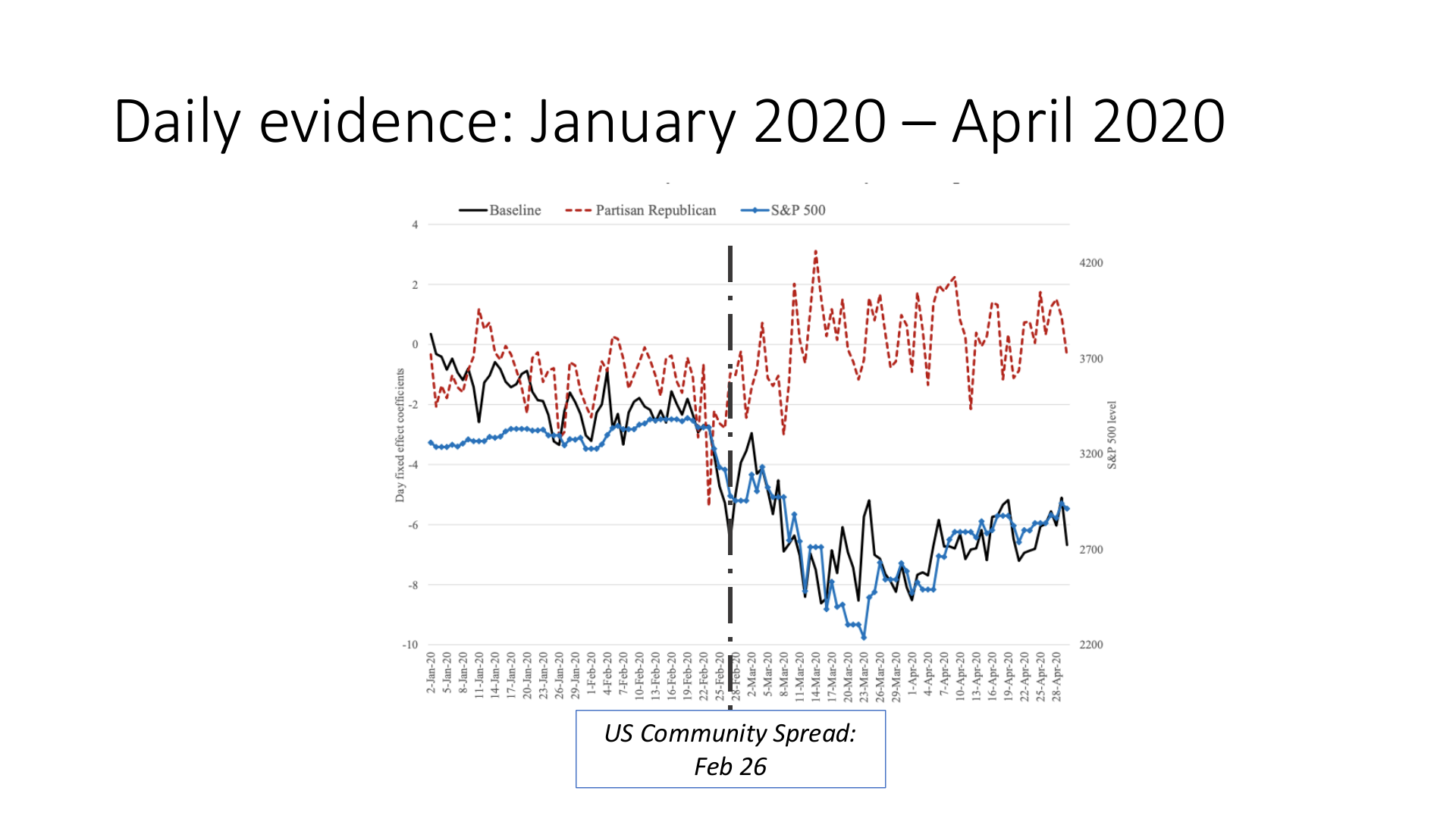

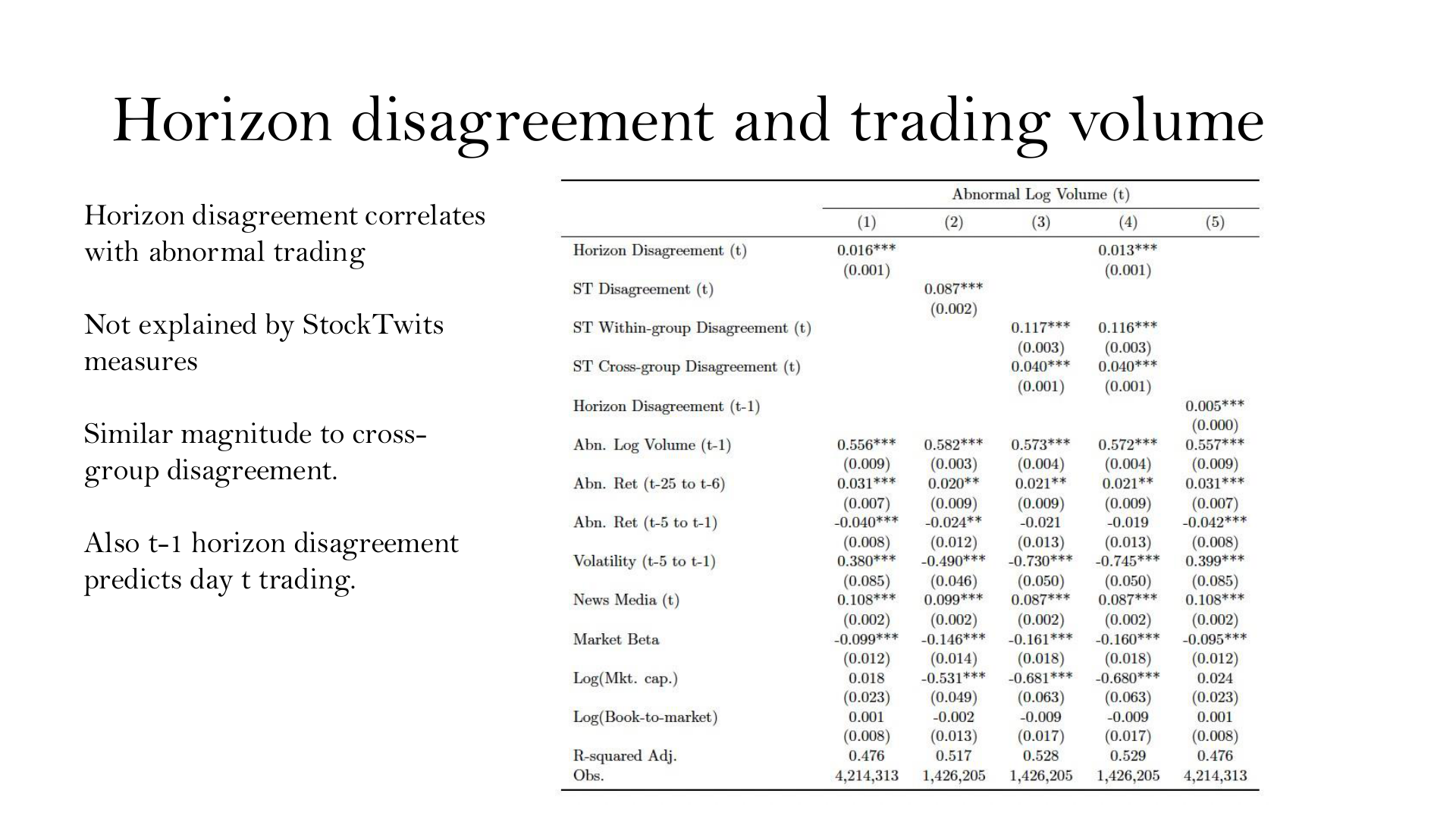

Social media is not merely a source of financial noise — it is a window into investors' deeper beliefs, identities, and reasoning styles. This session develops the "social media as a lens" approach, in which the abundant, high-frequency data generated by investors' online activity is used to study questions that were previously unanswerable. Three original papers illustrate the approach. Cookson and Niessner (2020, JF) exploit self-labeled bullish and bearish posts on StockTwits to construct a daily measure of investor disagreement, showing that differences in investment philosophy — fundamental versus technical — account for a large share of trading volume. Cookson, Engelberg and Mullins (2020, RAPS) show that partisan identity shapes investment beliefs even when the stakes are high: partisan Republicans maintained substantially more optimism than others throughout the COVID-19 pandemic. Cookson, Dim and Niessner use CAPS, the prediction platform of The Motley Fool, to measure investor horizons directly, finding that short- and long-horizon investors update their beliefs differently around earnings announcements, acquisition rumors, and market shocks — with horizon disagreement independently predicting trading volume.

Key themes

- Social media as a high-frequency survey: self-declared sentiment on StockTwits eliminates classification noise and enables new measures of investor disagreement

- Investment philosophy drives disagreement: fundamental versus technical investors persistently disagree, accounting for 34–65% of overall disagreement and a third of volume spikes around earnings

- Polarization reaches financial markets: partisan identity shapes investor beliefs in settings with direct financial stakes — a strong null hypothesis violated

- Horizons are directly measurable: CAPS (Motley Fool) provides explicit short- versus long-run predictions; short-horizon investors respond more strongly to earnings news and technical events

- Internal consistency validates the lens: language, event responses, and off-platform behavior all align with investors' declared identities

From the slides

Selected papers

- Cookson & Niessner (2020, JF) — "Why Don't We Agree?" — investor disagreement

- Cookson, Engelberg & Mullins (2020, RAPS) — "Does Partisanship Shape Investor Beliefs? Evidence from the Covid-19 Pandemic"

- Cookson, Dim & Niessner (2025, WP) — "Disagreement on the Horizon" — CAPS data

- Diether, Malloy & Scherbina (2002) — Analyst forecast dispersion

- Hong & Stein (1999) — Gradual information diffusion

- Gentzkow & Shapiro (2010) — Partisan media; iterative keyword method

- Avery, Chevalier & Zeckhauser (2016) — CAPS data

Data resources

- Cookson-Niessner disagreement measures — firm-day 2010–2021 (StockTwits)

- StockTwits — bullish/bearish self-labeled posts; API (restricted) or commercial

- CAPS (Motley Fool) — prediction data with explicit horizons; contact authors

- RavenPack — earnings announcements, technical signals, M&A events (commercial)

Social transmission bias and social media signals

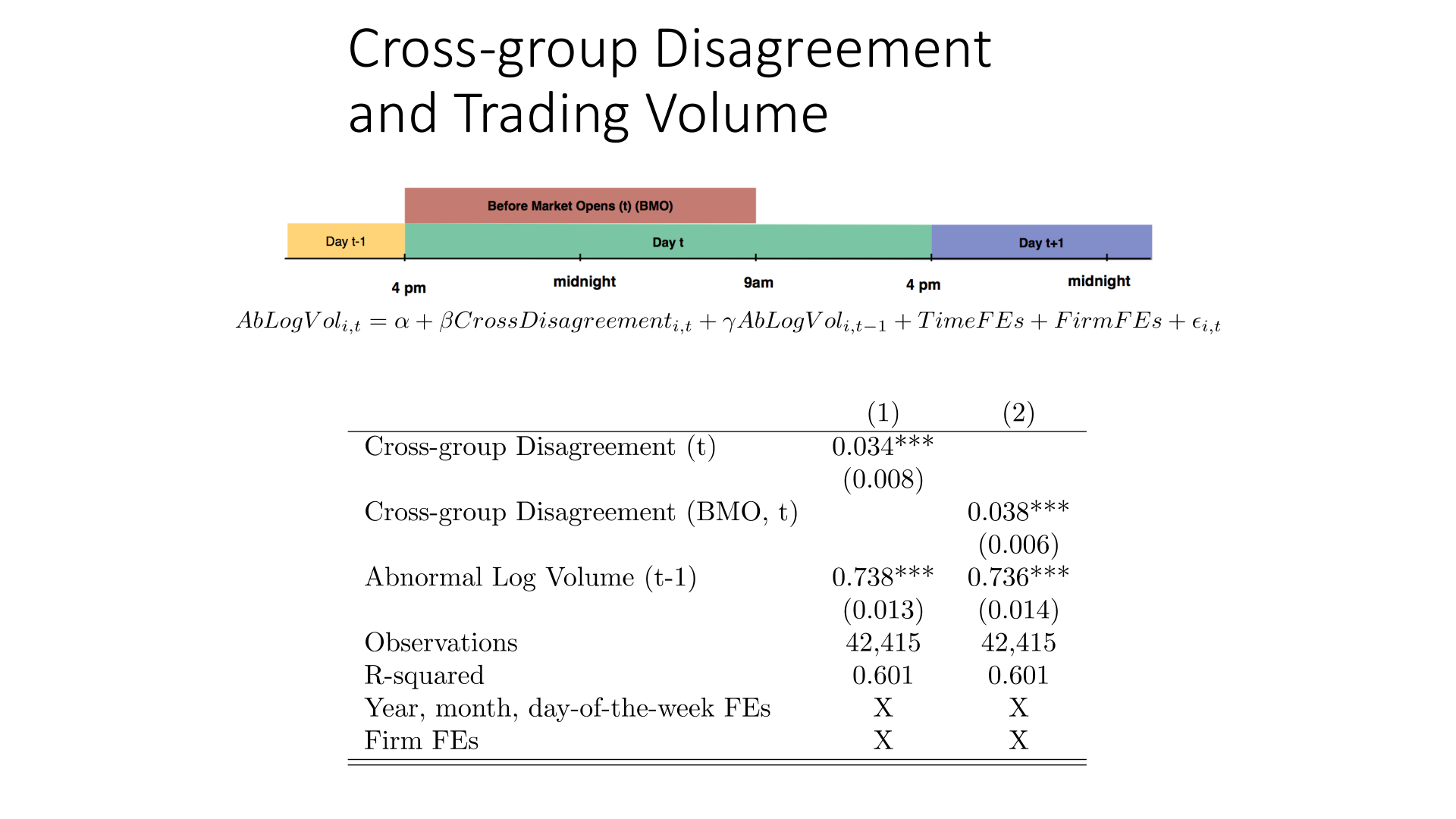

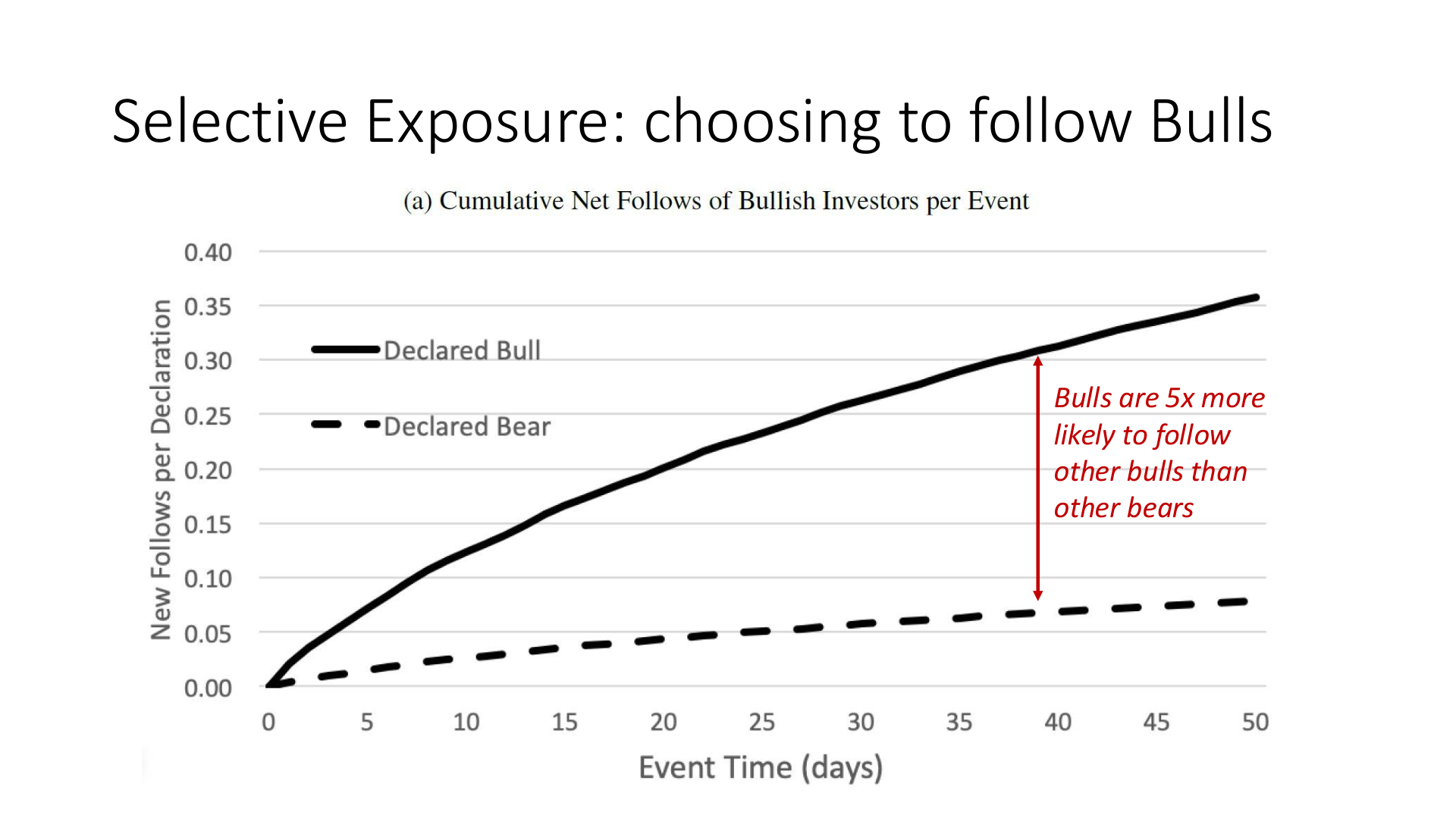

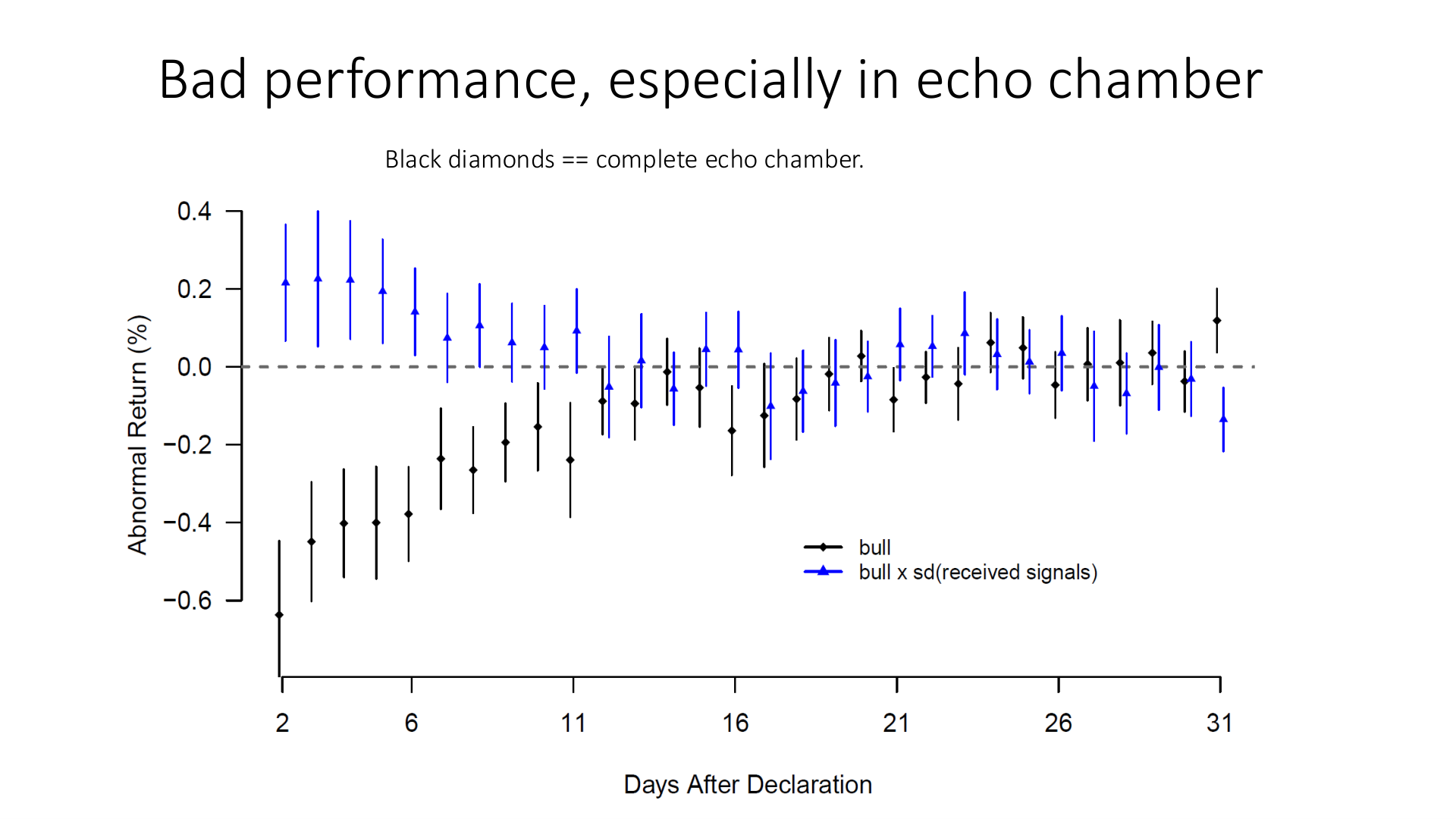

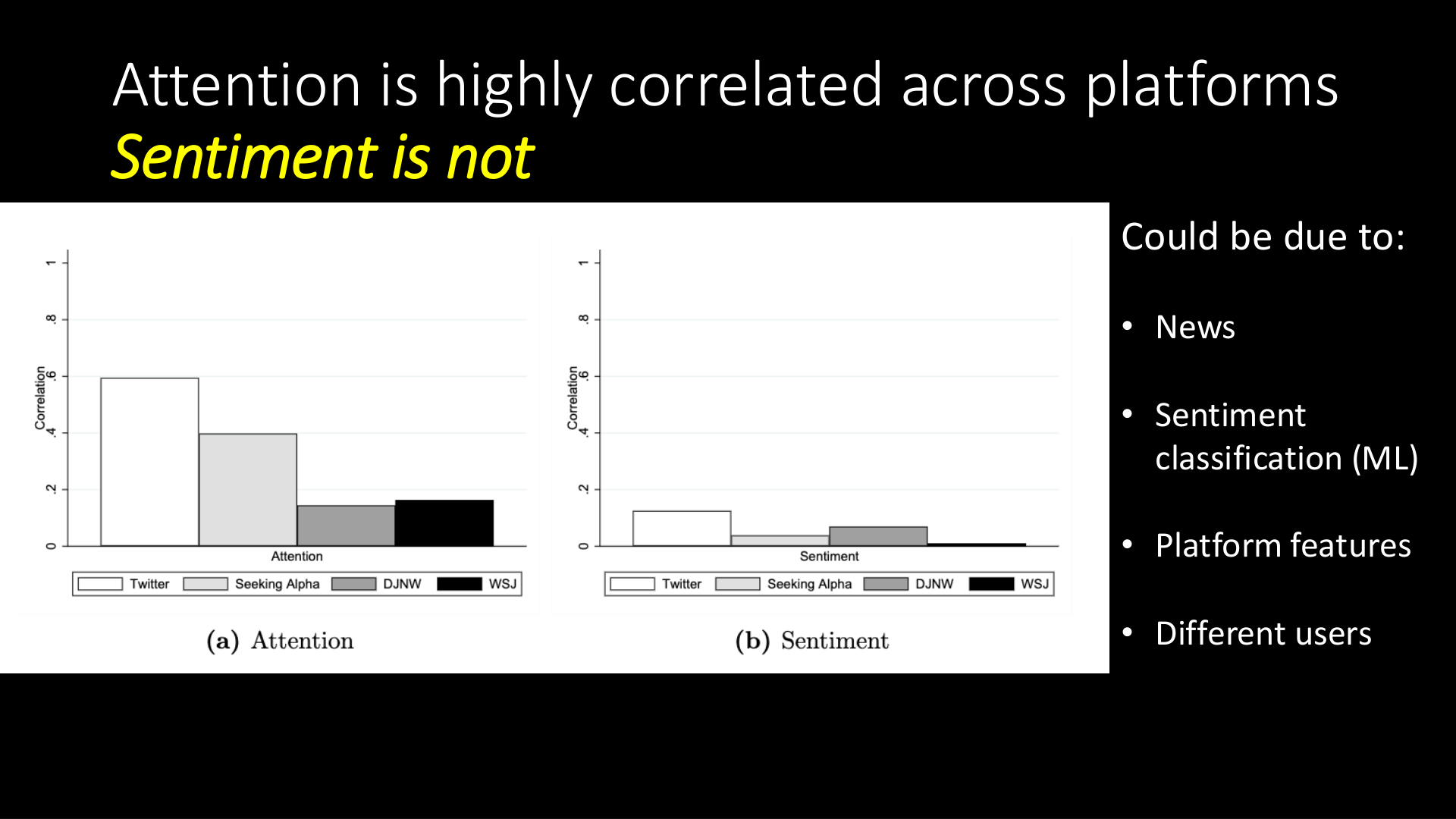

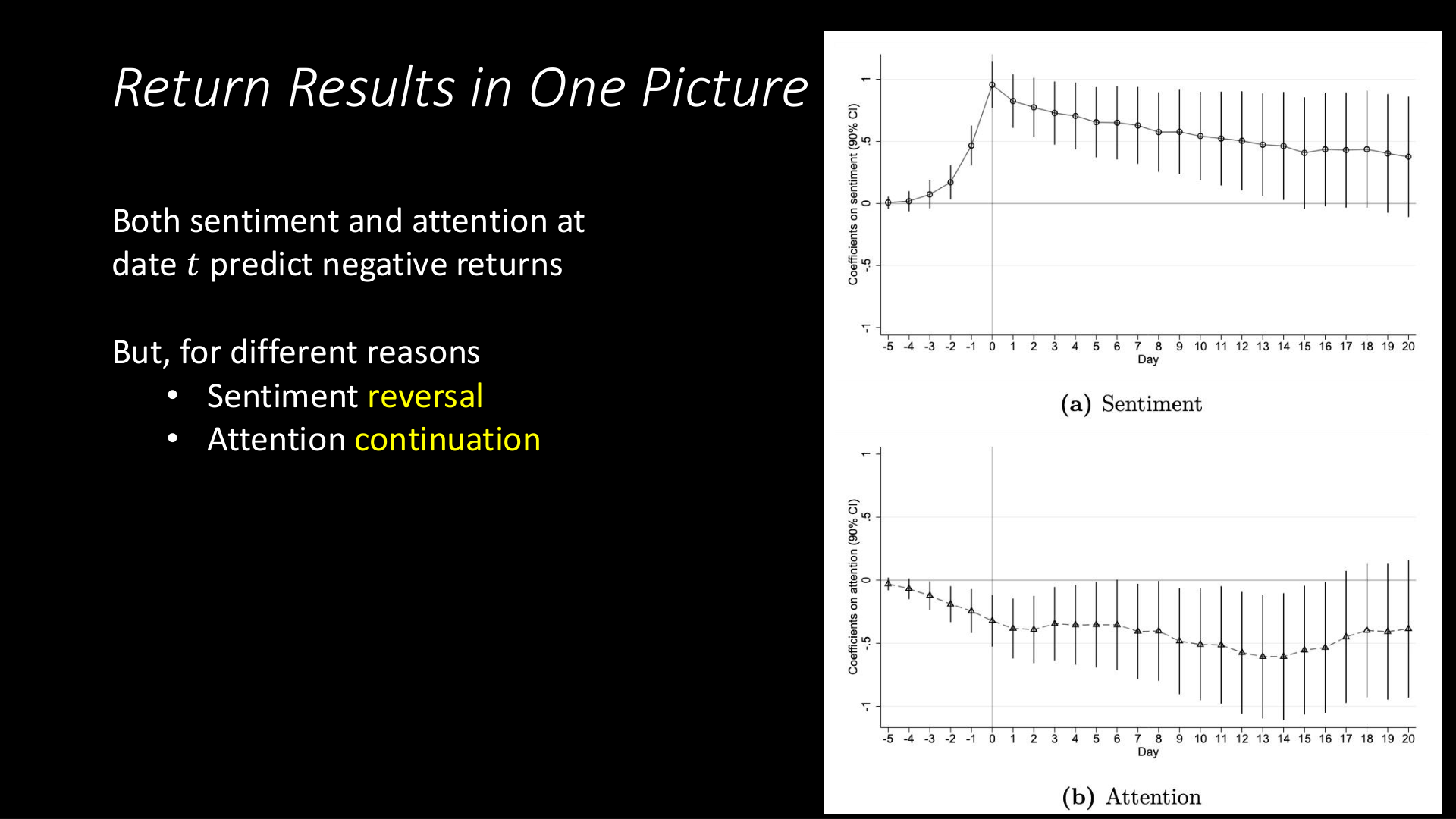

Social media does not merely reflect investor beliefs — it also shapes them, through selective exposure, information cascades, and the formation of echo chambers. This session examines the social transmission of information and its consequences for market efficiency, then turns to the problem of extracting reliable signals from social media data. The first half focuses on echo chambers: Cookson, Engelberg and Mullins (2023, RFS) show that investors on StockTwits are five times more likely to follow users who share their views, that the resulting information silos generate worse stock picks, and that echo chambers independently account for a large share of aggregate trading volume — suggesting that selective exposure sustains the very disagreement that drives markets. The second half examines cross-platform signal extraction. "The Social Signal" (Cookson, Lu, Mullins and Niessner, 2024, JFE) shows that investor attention is common across platforms while sentiment is platform-specific, with sharp implications for return predictability. At the market level, Cookson, Lu, Mullins and Niessner (WP) show that aggregate sentiment and attention both predict negative future returns — through distinct dynamics.

Key themes

- Echo chambers sustain disagreement: selective exposure creates information silos that keep bulls and bears persistently apart — solving the puzzle of why disagreement persists

- Information silos have consequences: users in echo chambers earn worse returns; echo chambers amplify aggregate trading volume at a magnitude comparable to disagreement itself

- Attention is monolithic; sentiment is not: across StockTwits, Twitter, and Seeking Alpha, investor attention co-moves strongly while sentiment is platform-specific — platforms are complements, not substitutes

- Platform features and user composition determine signal quality: the StockTwits character limit expansion improved sentiment predictability; the GME influx of new users destroyed it

- Market-level signals have distinct dynamics: aggregate sentiment predicts a within-month return reversal; aggregate attention predicts return continuation — the strategy yields a Sharpe ratio above 1.0

From the slides

Selected papers

- Cookson, Engelberg & Mullins (2023, RFS) — "Echo Chambers"

- Cookson, Lu, Mullins & Niessner (2024, JFE) — "The Social Signal"

- Cookson, Lu, Mullins & Niessner (WP) — Market signals from social media

- Chinco (2023, MS) — "The Ex Ante Likelihood of Bubbles"

- Kakhbod et al. (2025, WP) — "Finfluencers"

- Dim (2025, JFQA) — Seeking Alpha author skill

- Baker & Wurgler (2006) — Market-level investor sentiment

Data resources

- The Social Signal — firm-day sentiment and attention data (Cookson, Lu, Mullins & Niessner)

- StockTwits — follow graph and bullish/bearish posts; needed for echo chamber replication

- Social Market Analytics — firm-day Twitter sentiment (commercial)

- Seeking Alpha via RavenPack 1.0 — firm-day attention and sentiment (commercial)

- BJZZ retail trading imbalance — standard measure for validation

Consequences and real effects

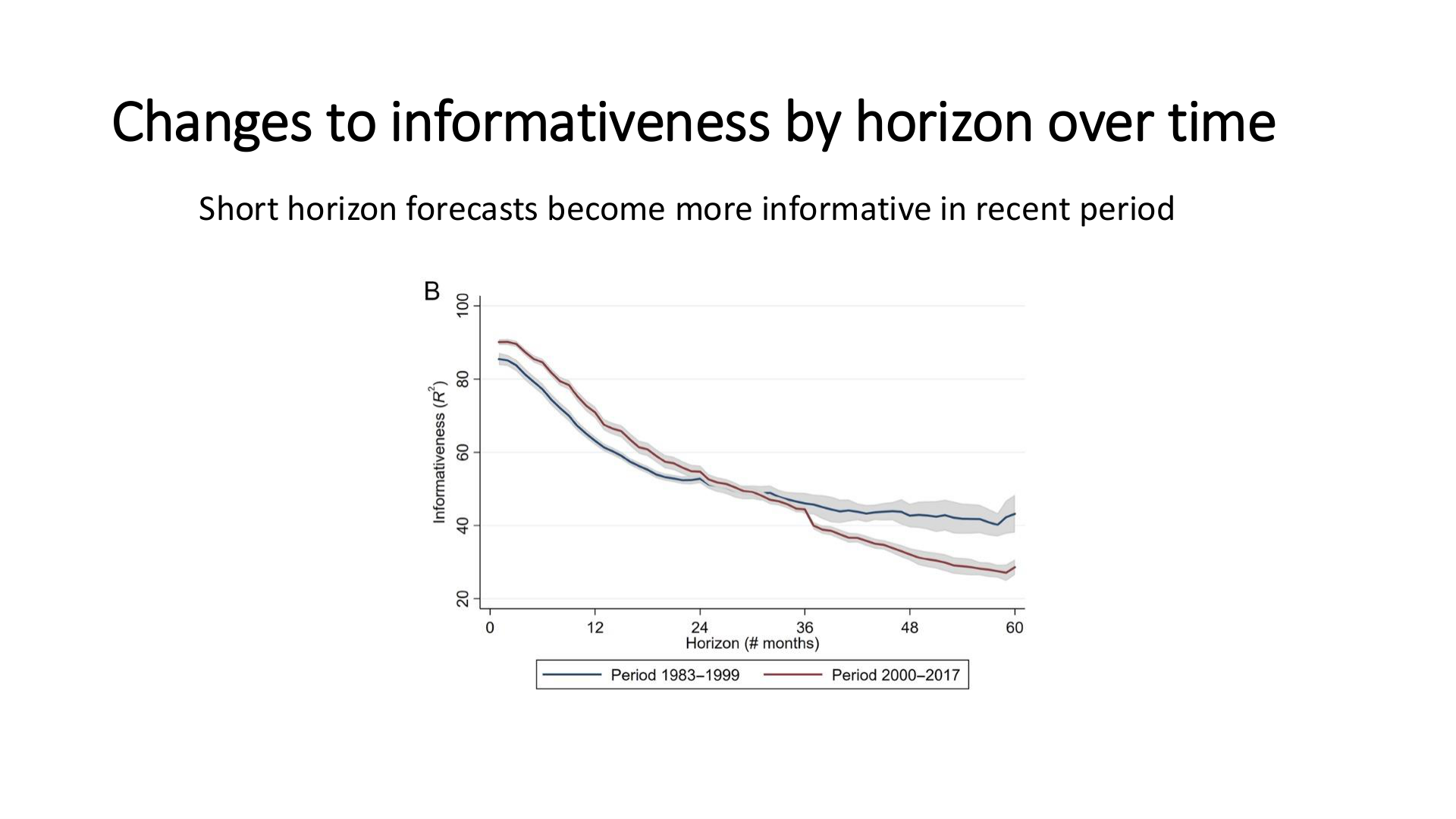

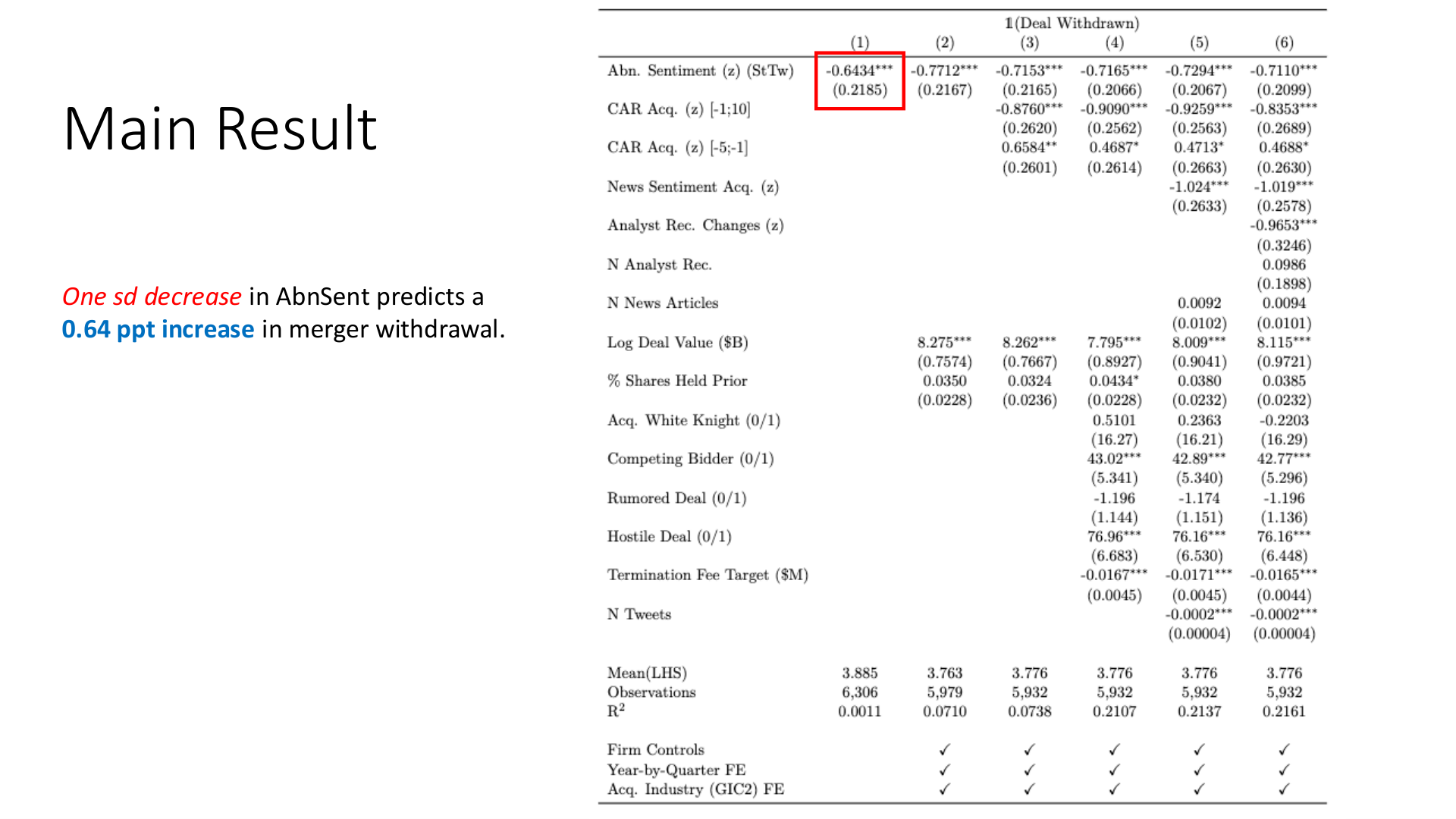

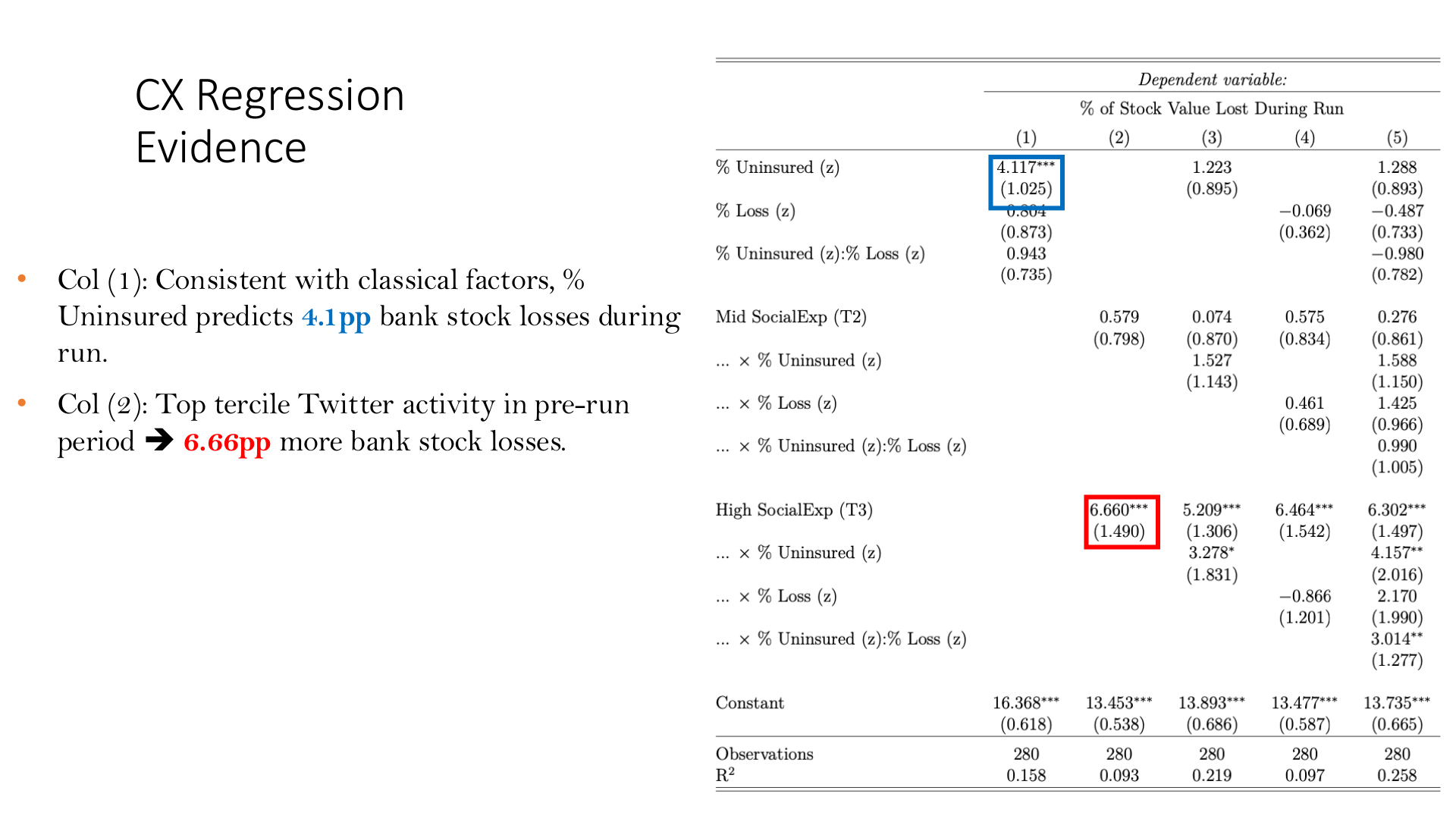

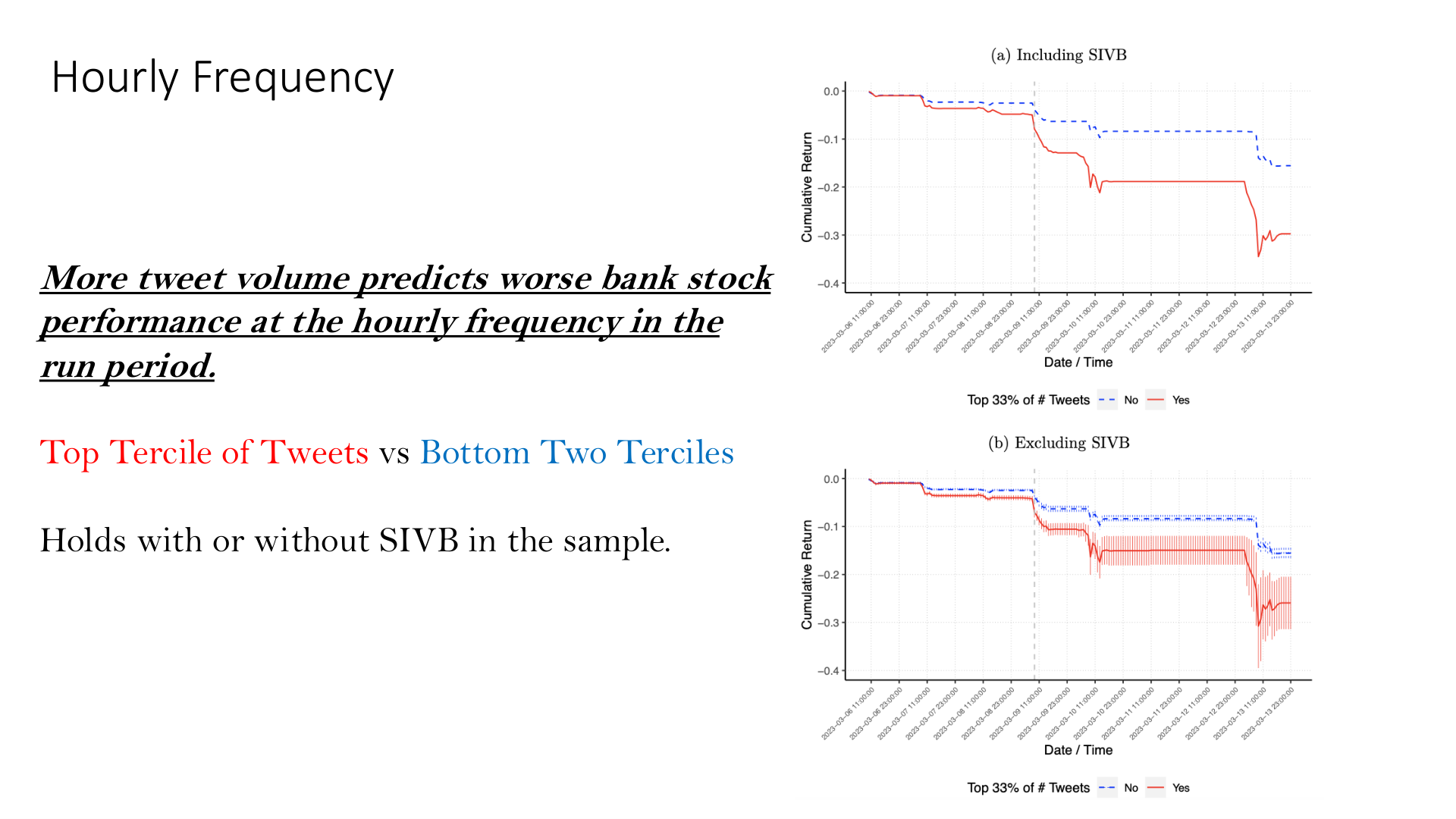

The consequences of social media extend beyond individual investor behavior into the structure of information production, corporate decision-making, and financial stability. This session examines three channels through which social media produces real effects. Dessaint, Foucault and Frésard (2024, JF) show that the entry of social media into a firm's information environment shifts analyst forecasts: short-horizon forecasts become more informative while long-horizon forecasts deteriorate, consistent with social media being a short-horizon information source. Cookson, Niessner and Schiller (2026, JF) ask whether social media feeds back into corporate decisions, using M&A deal withdrawals as a setting; they find that post-announcement social media sentiment predicts withdrawal at a magnitude comparable to the market's own price signal, and the effect is strongest when managers have the most to learn from external information. Finally, Cookson, Fox, Schiller, Gil-Bazo and Imbet (2026, JFE) study the collapse of Silicon Valley Bank — the first social media bank run — showing that pre-existing Twitter exposure amplified classical bank run risk factors, with top-tercile exposure predicting larger stock losses than a one-standard-deviation increase in uninsured deposits.

Key themes

- Social media reshapes information production: analyst short-horizon forecasts improve as social media coverage expands, while long-horizon forecasting quality declines

- Social media feedback is not a sideshow: post-announcement investor sentiment predicts M&A withdrawal at parity with cumulative abnormal returns — corporate managers are listening

- SVB as a case study in contagion: social media is a coordination technology whose broad reach amplifies traditional financial fragility; Twitter pre-exposure mattered more than uninsured deposits

- Listening infrastructure matters: firms with active corporate Twitter accounts show stronger sensitivity to the social media signal, consistent with deliberate monitoring

- The frontier: LLMs, TikTok and Discord, GIF and emoji sentiment, and connections between social media and the real economy remain open research territory

From the slides

Selected papers

- Dessaint, Foucault & Frésard (2024, JF) — "Does Alternative Data Improve Financial Forecasting?"

- Cookson, Niessner & Schiller (2026, JF) — "Can Social Media Inform Corporate Decisions? Evidence from M&A Withdrawals"

- Cookson, Fox, Schiller, Gil-Bazo & Imbet (2026, JFE) — Social media as a bank run catalyst

- Kogan, Moskowitz & Niessner (2023, RF) — Fake news and asset prices

- Bradley et al. (2024, RFS) — Information quality after GameStop

- Pedersen (2022, JFE) — GameStop and retail coordination

Data resources

- StockTwits firm-day sentiment (2010–2021) — continuous sentiment score

- Twitter API — cashtagged tweets and keyword search; user-level details

- Bank-level Twitter pre-exposure data — replication data for Cookson et al. (2026, JFE)

- FDIC / FFIEC Call Reports — uninsured deposits and balance sheet data (public)

- FirstRate Data — minute-level stock prices (commercial)

- Social Market Analytics — firm-day Twitter sentiment (commercial)