Slides

In-Class Demos

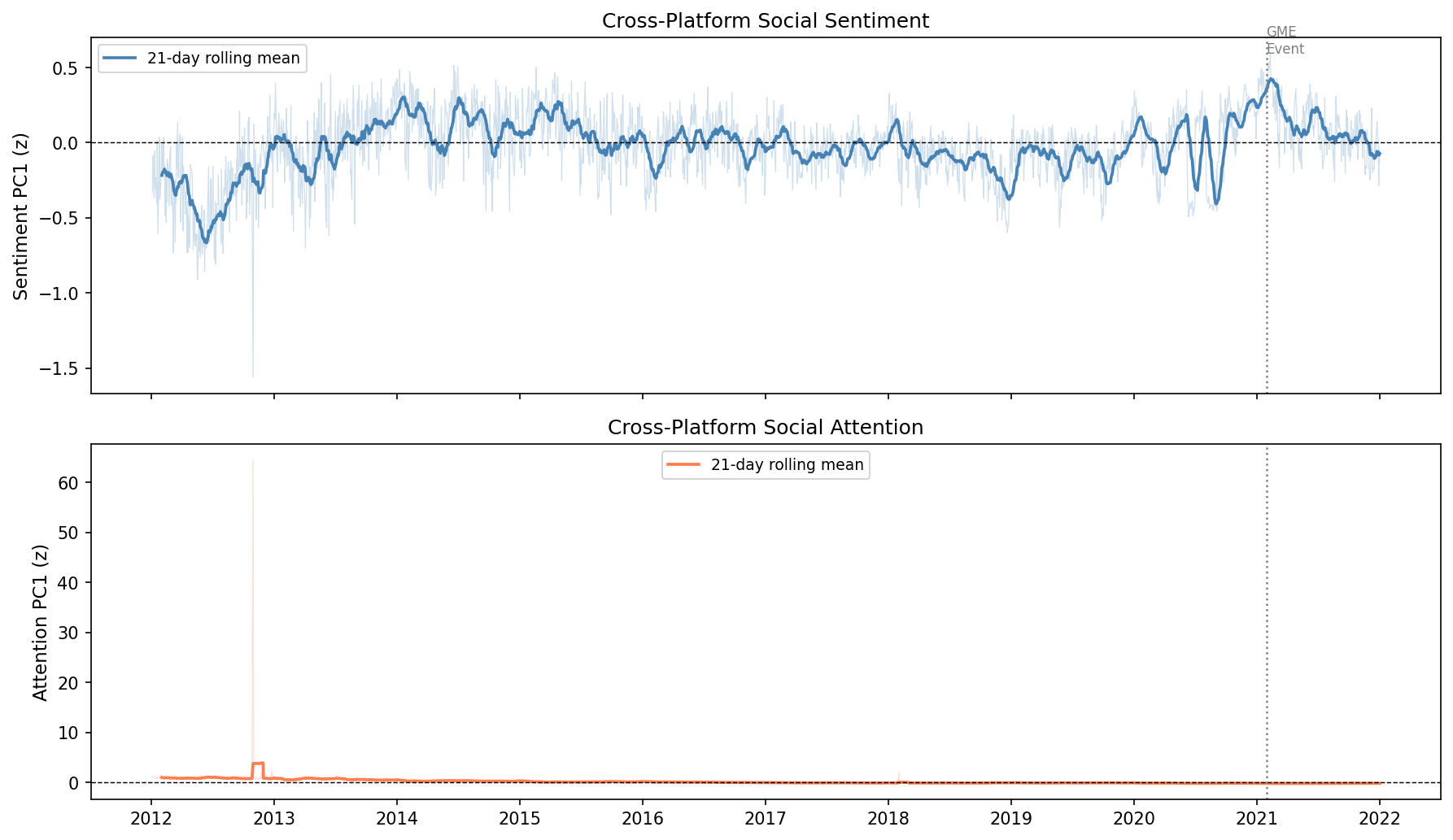

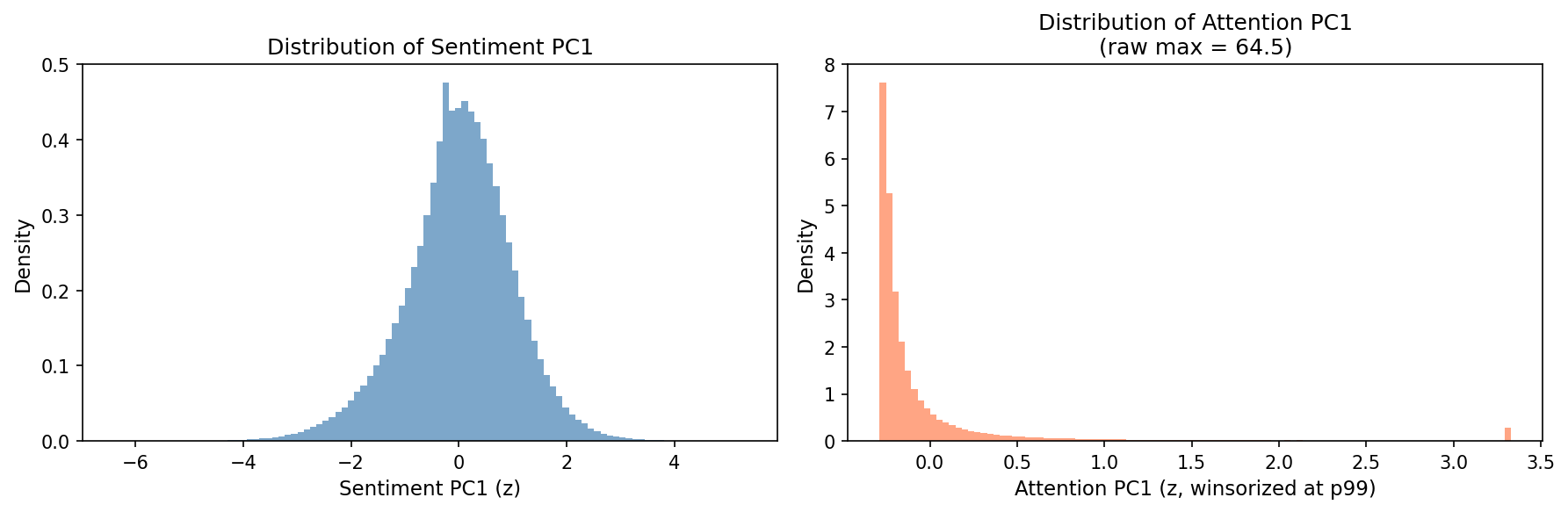

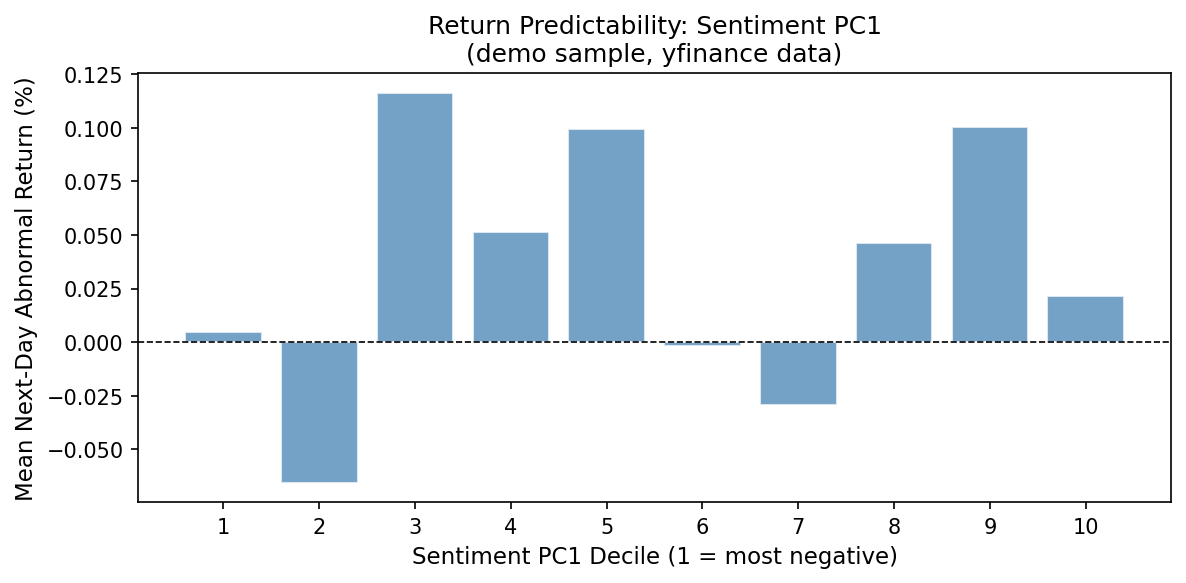

Demo 1 — Social Signal: Stock-Level Analysis

Starting from 821,534 firm-day observations from The Social Signal (Cookson, Lu, Mullins & Niessner, JFE 2024), a single Claude Code session produces a publication-style stock-level analysis in under 15 minutes. The researcher supplied the economic questions; Claude supplied the mechanics.

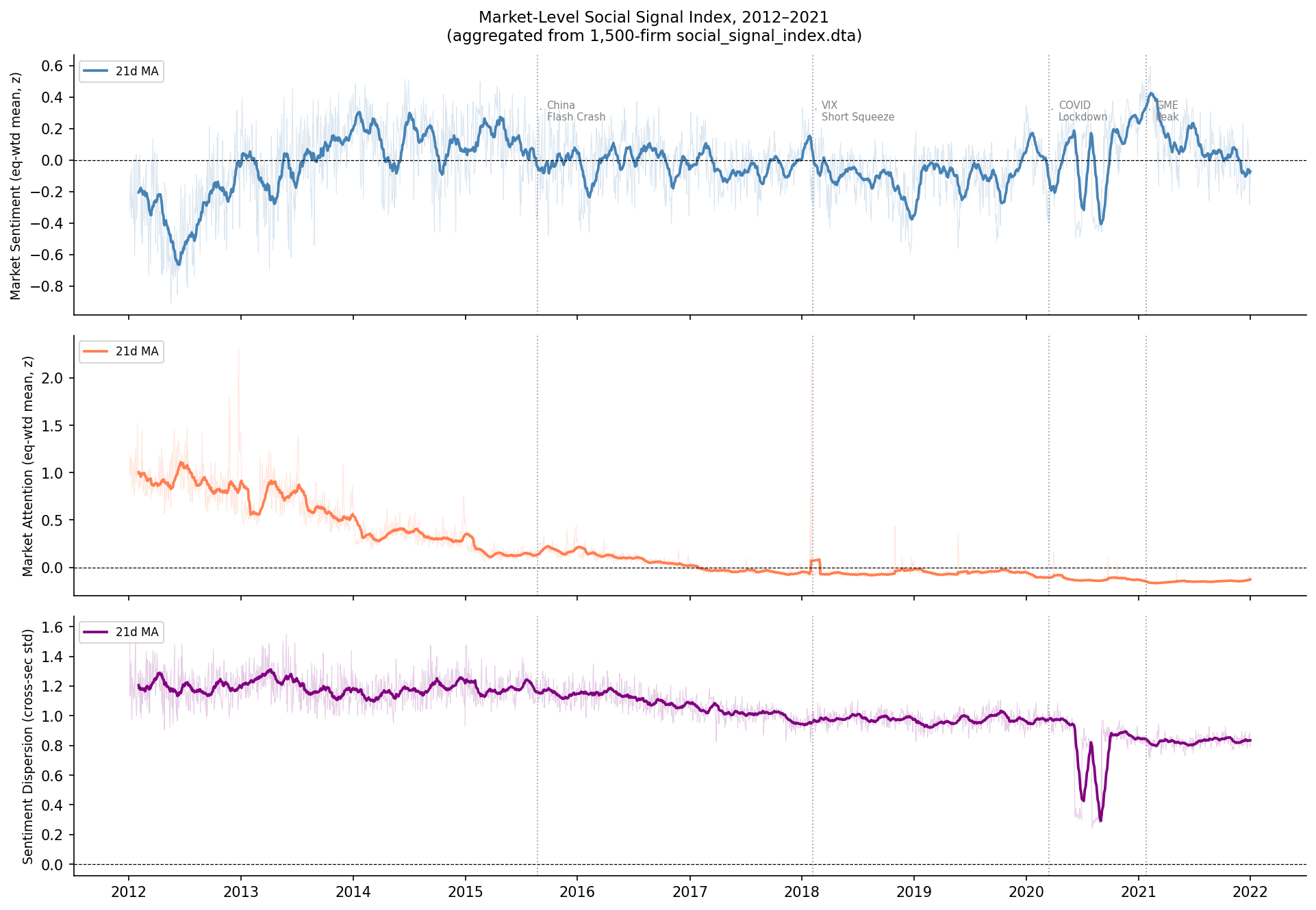

Demo 2 — Market-Level Analysis

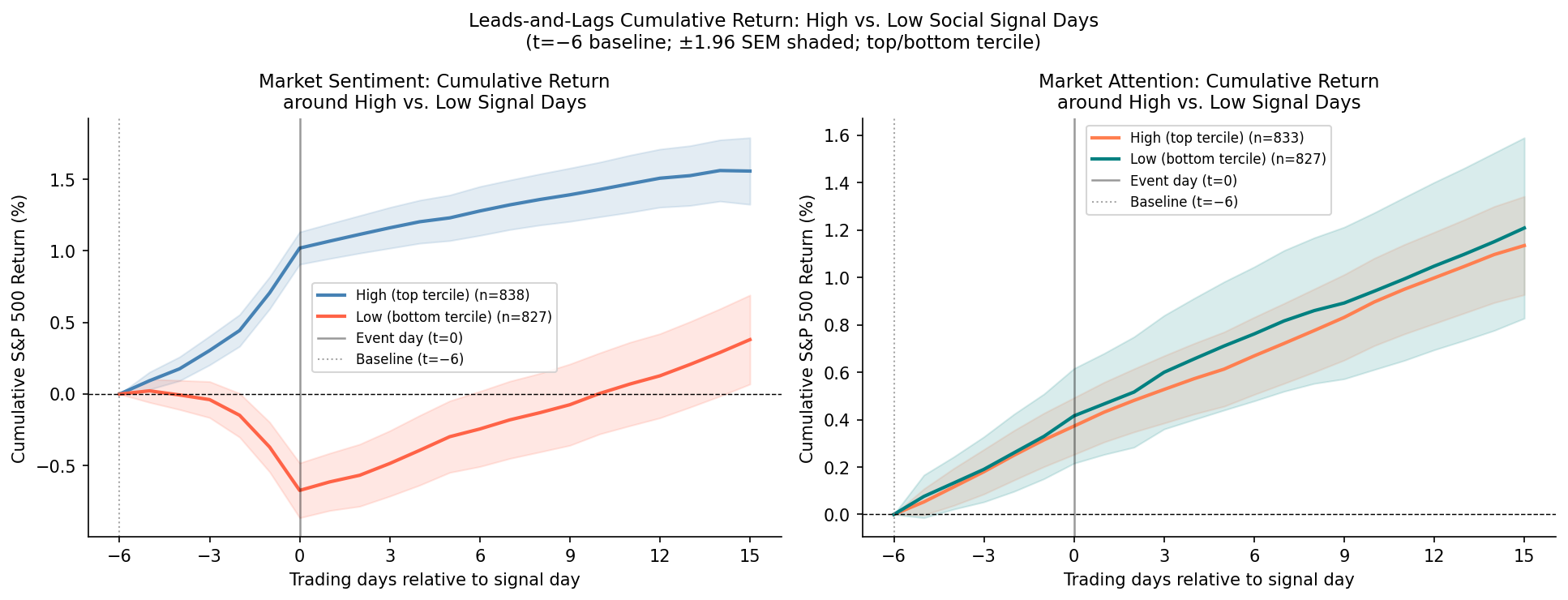

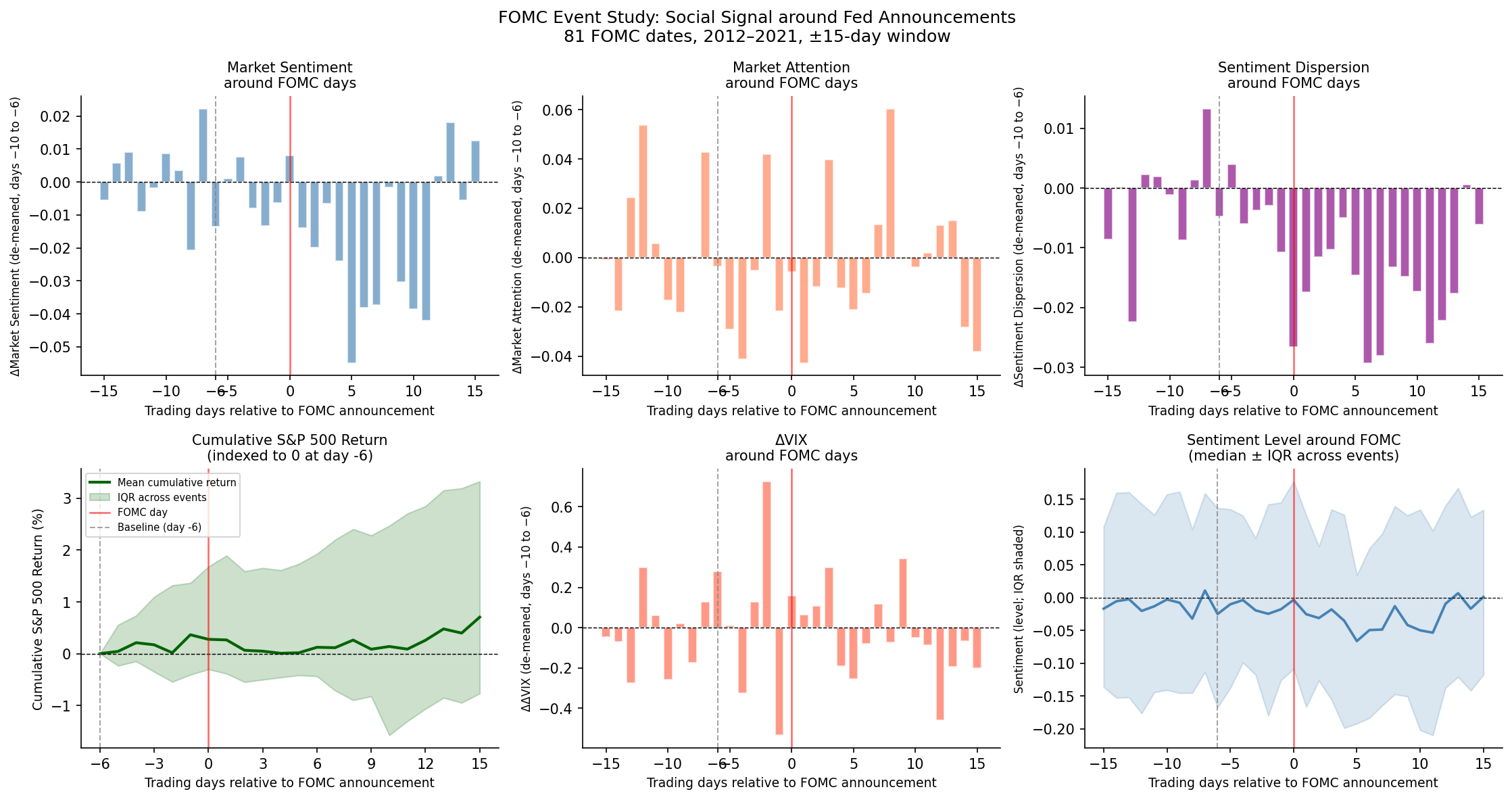

Four plain-English prompts build a complete market-level analysis from the same data: time-series properties, predictive regressions, a leads-and-lags event study, an FOMC event study, and a cap-weighted robustness check. See the demo guide for the full prompt sequence and methodology notes.

Resources

AI in Econ Wiki — curated by Mihail Velikov (Penn State Smeal): velikov-mihail.github.io/ai-econ-wiki